Sudan is making progress as it reconnects with the global economy, but patience is needed as the country seeks to tackle shortages and attract investment, the head of the World Bank said on his visit to the country.

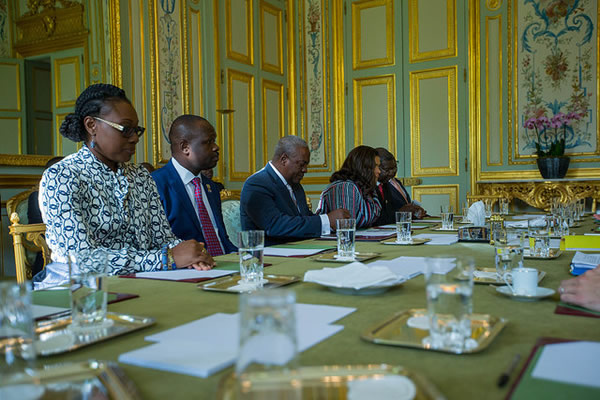

David Malpass landed in capital Khartoum late on Wednesday in what is the first visit for a World Bank president to the East African nation in more than 50 years, according to Sudanese prime minister’s office.

Sudan’s economy has been mired in a crisis that led to the overthrow of former leader Omar al-Bashir in 2019 and has continued since.

Last month, inflation slowed slightly to 388 percent and a sharply devalued currency has shown signs of stabilising, but many Sudanese are struggling with poverty, shortages of medicines, and power cuts.

Last week, authorities said they had thwarted an attempted coup, and on Thursday civilian groups are calling for pro-democracy protests in Khartoum.

“Sudan is making a transition from a violent situation, from a situation of shortages, to the situation that is gradually improving,” Malpass said after meeting Sudanese Prime Minister Abdalla Hamdok on Thursday.

“It takes time to go through this process and it will be important for people to approach it with patience and with tolerance for each other knowing that the whole that Sudan’s building – a nation – is going to be stronger than the individual parts.”

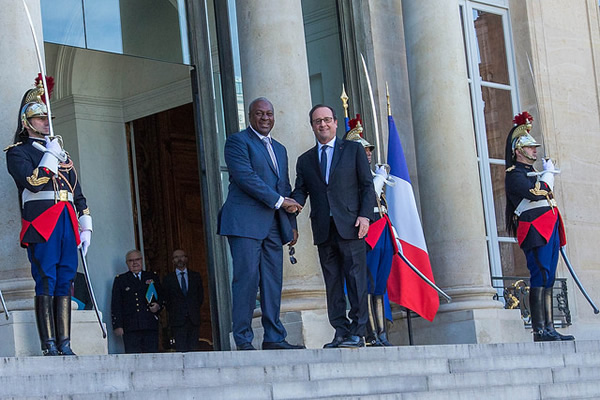

Malpass met Hamdok and Finance Minister Gibreil Ibrahim, who hailed the visit as a sign that Sudan’s integration into the international community “is progressing in strides”, the prime minister’s office said.

Economic hardships

Sudan has, for years, struggled with an array of economic woes, including a huge budget deficit and widespread shortages and soaring prices for essential goods.

Conditions worsened after the oil-rich south seceded in 2011 after decades of war, taking with it more than half of public revenues and 95 percent of exports.

Sudan also faced extensive international sanctions under al-Bashir.

Earlier this year, Sudan paved the way for extensive relief on more than $50bn in foreign debt by enacting rapid economic reforms, unlocking access to international financing.

During the next year, the World Bank says it will commit about $2bn in grants to help tackle poverty and inequality, and boost growth.

Source: News Agencies